Is banking system moving towards liquidity deficit? What it means for your loans, EMIs

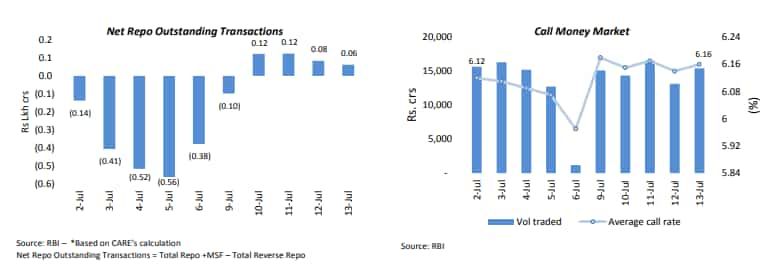

Net liquidity position has moved from a liquidity surplus level in the preceding week to a marginal liquidity surplus level in the week ended 13 July.

The concept of liquidity is a very important term for banks and the Reserve Bank of India. This term also impacts consumers in many ways. Liquidity is derived as the bids for reverse repo and repo in the LAF (Liquidity Adjustment Facility) auction, Term repo auction, Marginal Standing Facility (MSF) held by the RBI. Every lender has to maintain a cash balance with RBI which is based upon the CRR (Cash Reserve Ratio). From the way the things here are panning out, it looks like the banking system is moving towards a liquidity deficit, as per the recent data that has been published by Care Ratings. It needs to be noted that, this liquidity deficit will have its effect on RBI monetary policy and your lending rates.

Net liquidity position has moved from a liquidity surplus level in the preceding week to a marginal liquidity surplus in the week ended 13 July. The net liquidity surplus increased from Rs 0.1 lakh crore on 2 July to Rs. 0.4 lakh crore on 6 July following which lower reverse repos has put marginal pressures on liquidity.

Average call money rate for the week was 9 bps higher from that in the preceding week and average daily volume traded was 22% higher at Rs.14,922 crores.

Care Ratings said, “The average volumes traded in the call money market has increased on account of net liquidity deficit in the system and requirement of fortnightly reporting for the banks.”

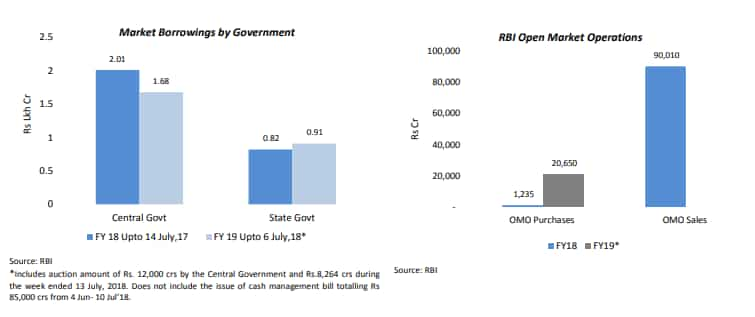

Meanwhile, central government auctioned securities worth Rs.12,000 crs on 13 July’18, while 10 state governments auctioned a total of Rs.8,264 crs via state development loans (SDLs) on 10 July’18. This has been lower during the current year compared to the previous year.

Further, RBI did not undertake any OMO operations during the week ended 13 July’18. The RBI has purchased securities amount to Rs.20,650 crs by way of open market operation in the current fiscal, notably higher than the Rs. 1,235 crs purchased in FY18.

Moreover, Treasury-bill yields for 91 days have rose by 19 bps during the week after witnessing a decline during the previous week. T-bill yields for 364 days has marginally moved up by 4 bps during the week.

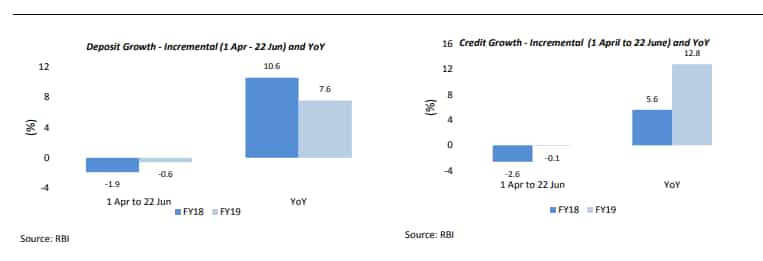

Incremental bank credit growth in FY19 (1 Apr-22 Jun) is (-) 0.1% compared with the growth of (-)2.6% in the comparable period last year. Likewise, the incremental bank deposit growth is (-0.6%) in FY19 (1 Apr-22 Jun) compared with (-1.9%) in the comparable period in FY18.

There are many reason that impact liquidity, one of which is RBI’s actions of buying and selling bonds, buying and selling currencies, and accepting bids for repo and reverse repo in the LAF auction.

The higher the CRR and SLR, the lower will be the liquidity system of the banks as they have to maintain more cash balances with the RBI and they have to buy more government bonds to hold.

The same way higher repo rate and reverse repo rate takes liquidity towards deficit,as banks borrow less from the RBI or lend more to the RBI. This in return will take the credit demand down on higher borrowing costs leading to lower deposits for banks.

If borrowing cost is higher, than interest payment on credit cards and loan get more expensive. This discourages people in terms of borrowing and spending. The ones who have existing loans will see less disposable income as they will spend more on interest payments.

If this is the case, then your EMIs are set to get higher. An EMI is a fixed amount of money that a borrowers needs to pay on a monthly basis to lenders or financial institutions, towards the loan amount they have taken.

05:25 PM IST

Explained | RBI allows reversal of liquidity measures under both SDF, MSF on weekends, holidays: What does it mean?

Explained | RBI allows reversal of liquidity measures under both SDF, MSF on weekends, holidays: What does it mean? RBI may not cut key lending rate before Feb unless inflation skids, global crisis hits: Axis Bank's Neeraj Gambhir

RBI may not cut key lending rate before Feb unless inflation skids, global crisis hits: Axis Bank's Neeraj Gambhir Money Guru: What should investors look at while investing in ETFs? Swati Raina decodes with Mrin Agarwal

Money Guru: What should investors look at while investing in ETFs? Swati Raina decodes with Mrin Agarwal From key policy rates to GDP growth estimates —here are 10 key takeaways from February RBI MPC announcements

From key policy rates to GDP growth estimates —here are 10 key takeaways from February RBI MPC announcements