Q3FY23 Results: Strong loan growth, margin improvement to drive earnings for top banks; Sharekhan picks 7 stocks for gains

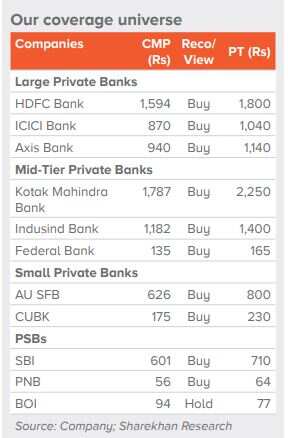

The domestic brokerage firm has picked Axis Bank, ICICI Bank, HDFC Bank, State Bank of India, Punjab National Bank, Federal Bank and AU Small Finance Bank as its preferred stocks

Banking sector will be in focus over the next two months as banks from private and public sector will begin announcing their October-December quarter results. India’s largest private lender HDFC Bank Limited will be the first one to declare its earnings on January 14, Saturday.

Brokerage firm Sharekhan has identified 12 stocks to frame its strategy on and expects gains between 13 and 31 per cent in these stocks. The stocks picked by Sharekhan are large private banks, mid-tier private banks, small private banks and public sector banks.

The domestic brokerage firm has picked Axis Bank, ICICI Bank, HDFC Bank, State Bank of India, Punjab National Bank, Federal Bank and AU Small Finance Bank as its preferred stocks.

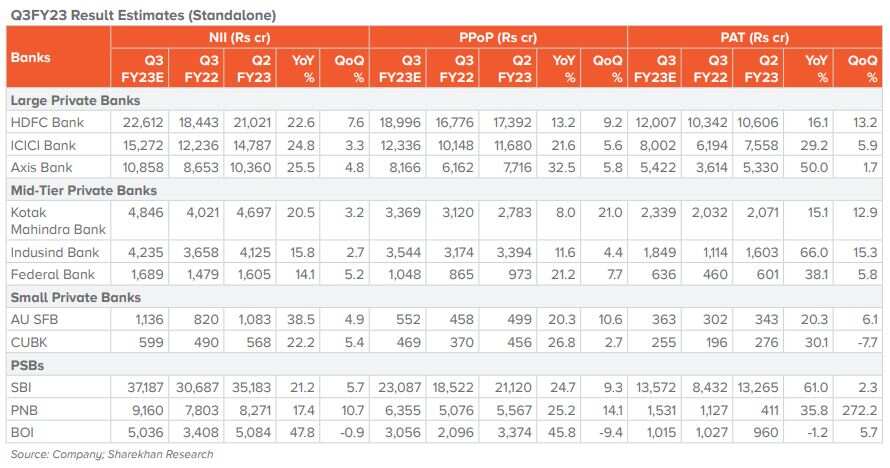

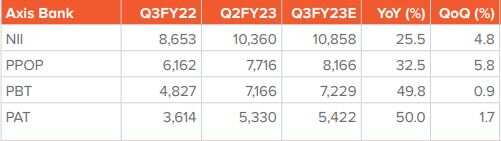

Sharekhan in its earnings preview said that HDFC Bank will likely report a 16.1 per cent YoY jump in net profit while ICICI Bank is expected to report 29 per cent jump. Third largest private lender Axis Bank is estimated to report a 50 per cent jump on the YoY basis. The Net Interest Income (NII) for these top private lenders is seen at 22.6-25.5 per cent.

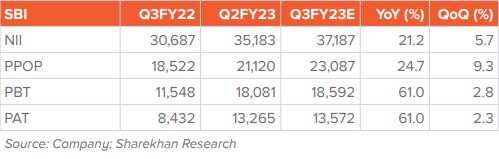

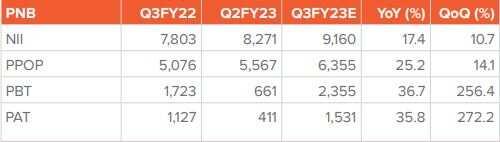

Among PSU Banks, SBI is expected to report 61 per cent jump in Profit After Tax (PAT) while PNB could see a 35 per cent increase in its net income. The NII for SBI is seen at 21.2 YoY while 17.4 for PNB.

Earnings Estimate Chart

Source: Sharekhan

Source: Sharekhan

Sharekhan’s Coverage Universe (Chart)

Sector Outlook

Sharekhan in a note said that the banking sector is expected to report a healthy performance in Q3FY23, led by strong loan growth, margin improvement and lower credit costs. Net Interest Income (NII) growth is likely to be strong on account of robust loan growth, while benign core credit cost would support earnings, it further said.

1) Deposits growth is expected to gain traction as deposit rates have risen sharply across banks over the past few months.

2) The banks will likely witness improvement in asset quality on moderation in slippages, healthy recoveries, and better collection efficiencies.

Headwinds

1) Global economic cycle and interest rate tightening witnessed across the globe could act as a dampener, it noted. The impact could be in the form of exchange rate volatility and excessive tightening in the local market.

2) Consensus estimates for GDP have been lowered for CY2023.

3) The quantum of margin expansion is expected to be lower compared to the previous quarter due to increased cost of deposits to garner a higher share of retail liabilities.

4) Slippages from the restructured book would be key monitorables.

5) There could be some slowdown in loan growth in FY2024E, which may be partially due to higher base effect and increased CD ratio, rather than on asset quality at this stage of the cycle.

Stocks to Buy

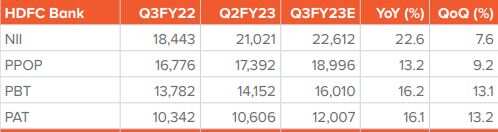

Buy: HDFC Bank | Upside: 13% | Target: Rs 1,800 | CMP: Rs 1570

The stock was recommended at trading price of Rs 1,800. NIM expected to improve sequentially while asset quality expected to remain stable. Investors must keep a track on regulatory dispensations.

Estimates Chart

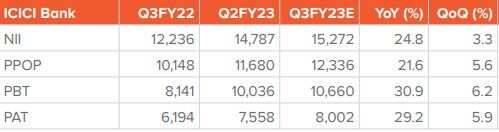

Buy: ICICI Bank | Upside: 20% | Target: Rs 1,040 | CMP: Rs 863

Advances are likely to grow by 20 per cent y-o-y, aided by broad based growth in all segments. NIMs likely to remain stable QoQ with positive upward bias. The key monitorable would-be deposit growth and margins outlook. The stock was recommended at a price of Rs 870.

Estimates Chart

Buy: Axis Bank | Upside: 21% | Target: Rs 1,140 | CMP: Rs

Advances expected to grow by 16 per cent y-o-y led by retail and SME. NIMs are expected to expand sequentially. The key monitorable would be the progress of the Citi portfolio and improvement in operating profit growth further led by some improvement in cost ratios. The stock was recommended at a price of Rs 940.

Estimates Chart

Buy: SBI | Upside: 18% | Target: Rs 710 | CMP:

Advances are likely to grow at 18 per cent y-o-y with margins likely to remain stable sequentially. Asset quality will also remain stable. Slippages would be largely from SME and retail book while corporate book will continue to hold well. The stock was recommended at a price of Rs 601.

Estimates Chart

Buy: PNB | Upside: 14% | Target: Rs 64 | CMP:

Advances growth will likely accelerate while margins are seen to remain stable sequentially. Key monitorable would-be deposit growth, margin outlook and slippages from restructured portfolio and ECLGS portfolio. The stock was recommended at a price of Rs 54.

Estimates Chart

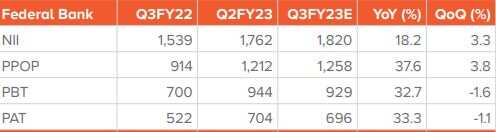

Buy: Federal Bank | Upside: 22% | Target: Rs 165 | CMP:

The stock was recommended at a price of Rs 135. Margins are to remain stable QoQ while key monitorable would be deposit growth outlook and any timelines of listing of Fed Fina (NBFC subsidiary).

Estimates Chart

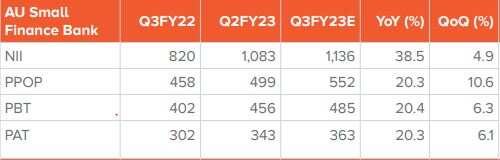

Buy: AUSFB | Upside: 28% | Target: Rs 800 | CMP:

The stock was recommended at a price of Rs 626. Margins are likely to remain stable QoQ. Key monitorable would be deposit growth outlook and any timelines of listing of Fed Fina (NBFC subsidiary).

Estimates Chart

(Disclaimer: The views/suggestions/advises expressed here in this article is solely by investment experts. Zee Business suggests its readers to consult with their investment advisers before making any financial decision.)

Get Latest Business News, Stock Market Updates and Videos; Check your tax outgo through Income Tax Calculator and save money through our Personal Finance coverage. Check Business Breaking News Live on Zee Business Twitter and Facebook. Subscribe on YouTube.

RECOMMENDED STORIES

04:36 PM IST

Anil Singhvi Market Strategy October 31: Important levels to track in Nifty50, Nifty Bank today

Anil Singhvi Market Strategy October 31: Important levels to track in Nifty50, Nifty Bank today Anil Singhvi Market Strategy October 30: Important levels to track in Nifty50, Nifty Bank today

Anil Singhvi Market Strategy October 30: Important levels to track in Nifty50, Nifty Bank today Anil Singhvi Market Strategy October 28: Important levels to track in Nifty50, Nifty Bank today

Anil Singhvi Market Strategy October 28: Important levels to track in Nifty50, Nifty Bank today Bandhan Bank Q2 FY25 Results: Profit jumps 30% to Rs 937 crore, beats expectations

Bandhan Bank Q2 FY25 Results: Profit jumps 30% to Rs 937 crore, beats expectations  Anil Singhvi Market Strategy October 25: Important levels to track in Nifty50, Nifty Bank today

Anil Singhvi Market Strategy October 25: Important levels to track in Nifty50, Nifty Bank today