Shares to buy today: Top IT stocks that investors can think of, say experts

Indian IT has ‘hit refresh’ with reinvention across multiple tech cycles and is now tuned to the all-encompassing and ubiquitous ‘Digital’ shift.

Recounting hits and misses in 3QFY19 for Indian IT and review both revenue and margin were in-line against the estimates at an aggregate level of the market experts. Revenue grew 2.2% QoQ (highest 3Q since FY14) and EBIT margins were flat. Within tier-1 IT, INFY and TechM posted relative revenue beat while LTI, Zensar & Sonata delivered rev beat within tier-2 IT. Margin outperformance was visible in Wipro, Persistent and Sonata while prominent misses on margins included eClerx and Zensar.

Giving an outlook of the Indian IT counters Apurva Prasad, Analyst, HDFC Securities & Amit Chandra, Analyst at HDFC Securities informed in a detail research study citing, "Indian IT has ‘hit refresh’ with reinvention across multiple tech cycles and is now tuned to the all-encompassing and ubiquitous ‘Digital’ shift. Initial success in transitioning to a new business model is evident in growth leadership against global peers (who led the cycle). We believe that even as digital portfolio and industry penetration is maturing, Indian IT’s investments (re-skilling, platforms & partnerships, acquisitions) will open up a larger addressable market with better pricing power."

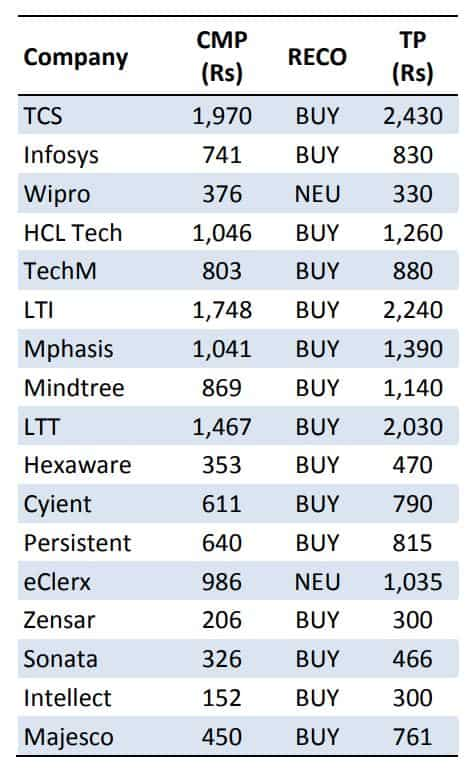

Please see below the counters report and outlook of the IT stocks by HDFC Securities research:

The key highlights of the research study are as follows:

1] Deal flows continue to strengthen, with (1) Strong industry-wide indicators (from ISG, DXC, Capgemini), (2) TCS’ TCV increased 20% over 1Q-2Q rate, gains vs. Accenture, (3) INFY’s large deal bookings at USD 1.57bn (50% of FY18 TCV), (3) Highest ever deal bookings (ex-renewals) by HCLT and Hexaware (USD 100mn+ net-new).

2] Guidance/outlook provided by management reflects continued strength with no signs of macro weakness ‘yet’. The notable increases in guidance came from Infosys, HCLT and LTTS. Digital continues to rise with improving margin supported by pricing and digital spend becoming more non-discretionary. TCS’ scale and growth leadership in digital continues.

3] Operating efficiencies (automation), pyramid rationalisation and pricing (in digital services) are strong offsets to margin headwinds from greater localisation and the tight US tech labour market. Tier-2 IT (PSYS, Mphasis, LTI, LTTS) are less prone to Brexit repercussions on portfolio composition (ceteris paribus).

4] TCS and INFY outperformed on client metrics (>USD100/10mn buckets). Headcount adds continue to accelerate with 70k increase in 9MFY19 as compared to 87k over FY17-18 for tier-1, with uptick in onsite hiring and escalating sub-contracting.

10:37 AM IST

Knee-jerk reaction: yes, but do wars wreak havoc on markets? Here is the data

Knee-jerk reaction: yes, but do wars wreak havoc on markets? Here is the data FIRST TRADE: Sensex slips over 600 pts, Nifty below 21,850; here's what is dragging the indices

FIRST TRADE: Sensex slips over 600 pts, Nifty below 21,850; here's what is dragging the indices  FIRST TRADE: Sensex gains over 280 pts, Nifty near 22,250; BPCL, Power Grid up over 3%

FIRST TRADE: Sensex gains over 280 pts, Nifty near 22,250; BPCL, Power Grid up over 3% FINAL TRADE: Sensex slips 456 pts, Nifty settles at 22,147.9 amid heavy selling in IT

FINAL TRADE: Sensex slips 456 pts, Nifty settles at 22,147.9 amid heavy selling in IT  FIRST TRADE: Sensex slips over 500 pts, Nifty below 22,150 amid geopolitical tensions; TCS, Infosys down over 1%

FIRST TRADE: Sensex slips over 500 pts, Nifty below 22,150 amid geopolitical tensions; TCS, Infosys down over 1%